This guide breaks down exactly what e-reporting is, who it applies to, what you must report, how often, and what happens if you get it wrong.

What Is E-Reporting in France?

E-reporting (e-reporting or transmission de données) is the obligation to electronically transmit transaction and payment data to the French tax administration for operations that are not covered by domestic B2B e-invoicing.

Put simply: if you cannot send a structured electronic invoice through the French invoicing ecosystem because the buyer is a private consumer, sits abroad, or is otherwise out of scope, you still owe the DGFiP visibility into that transaction. E-reporting is how that data reaches the authority. Reporting must be done through an approved platform, not by manual filing.

The one-line definition: E-invoicing handles the invoice itself between two French businesses. E-reporting handles the data about everything else, so the DGFiP still sees the full picture of your French VAT activity.

E-Reporting vs E-Invoicing: The Key Difference

This is the distinction that trips up most teams. They are two separate obligations, introduced together, but they apply to different flows.

Who Must Comply With E-Reporting?

The e-reporting obligation has a wider reach than many expect. It applies to:

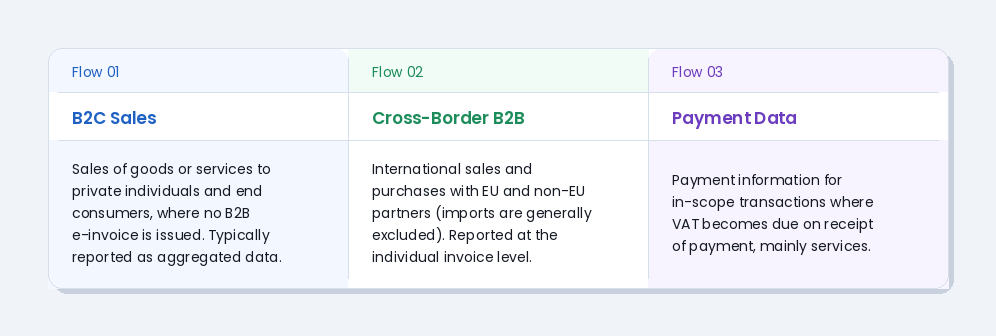

Businesses established in France that carry out transactions falling outside domestic B2B e-invoicing, for example a retailer selling to consumers or a company exporting goods.

Foreign and non-established businesses that are VAT-registered in France. Even without a permanent establishment in the country, these companies must still meet e-reporting obligations for their relevant French-taxable transactions. Note that under the Loi de Finances 2026, the issuance and e-reporting timeline for large and intermediate non-established taxpayers was deferred to September 2027.

The same phased calendar that governs e-invoicing applies: the obligation begins 1 September 2026 for large and mid-sized enterprises, and 1 September 2027 for small and micro-enterprises.

What Transactions Must Be Reported?

French authorities define three broad families of reportable activity.

Exempt or out-of-scope flows generally include OSS/IOSS distance sales and customs-handled imports and exports. Because classification drives both the reporting method and frequency, accurate tagging of each transaction type is essential, a small mapping error early on multiplies into many failed submissions later.

Payment Data Reporting Explained

Payment reporting is the most misunderstood layer. It does not apply to every transaction. It applies only where VAT is due upon collection of payment, which in practice means most services rather than goods.

Crucially, payment e-reporting excludes reverse-charge cases and suppliers who have opted for VAT on debits (TVA sur les débits). If your business operates on the debit basis, your payment-reporting burden is materially lighter, but you must be able to prove that status through your platform configuration.

Why this matters operationally: Payment data lives in your treasury and banking systems, not your invoicing module. Capturing it for e-reporting means your Plateforme Agréée must connect to more than just your ERP billing engine. This is exactly where weak integrations break.

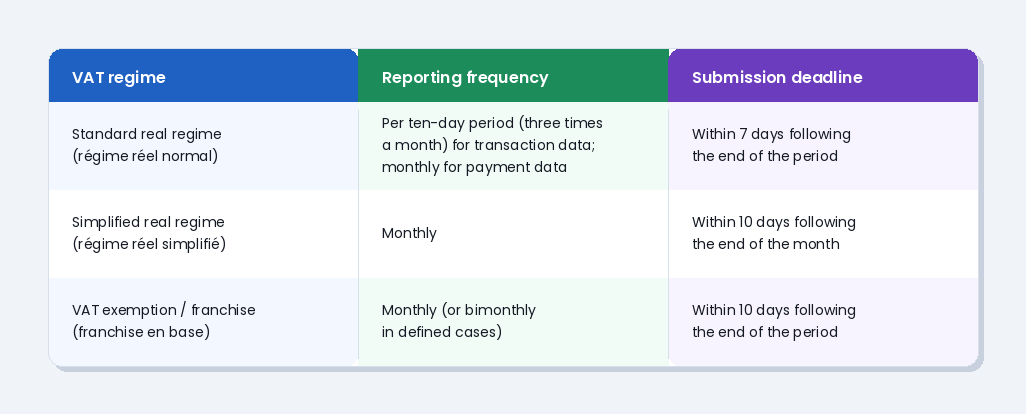

Reporting Frequency and Deadlines

Unlike e-invoicing, e-reporting data is not transmitted in real time. Frequency is tied to your VAT regime, and the deadlines are strict.

The standard cadence is once every ten days, with relief measures for SMEs. Because some specifics remain subject to forthcoming decrees, working with a platform that updates automatically is the safest position.

How E-Reporting Flows to the DGFiP (the Y-Model)

France uses a decentralised CTC architecture known as the Y-model. Invoices and reports are exchanged through accredited private platforms, the Plateformes Agréées (PA), while the data is funnelled to the tax authority through the Portail Public de Facturation (PPF), now formally the central directory (annuaire central).

Technically, e-reporting datasets travel to the PPF via a dedicated transmission channel often referenced as Flow 10 (F10), with a receipt mechanism confirming whether the submitted dataset was accepted or rejected. In short: your systems feed the PA, the PA validates and transmits, and the PPF routes the data onward to the DGFiP for VAT oversight.

A note on terminology: If you have read older guides referring to a PDP (plateforme de dématérialisation partenaire), the Loi de Finances 2026 renamed this to Plateforme Agréée (PA). Same role, new official name. Both terms still appear across the market during the transition.

Penalties for Non-Compliance

E-reporting carries its own penalty regime, separate from e-invoicing fines. Under the clarified 2026 framework:

A fine of €250 per missing or late e-reporting transmission, capped at €15,000 per year, applies to the B2C and cross-border transactions covered by e-reporting. France is moving from preparation to active enforcement, and using a non-accredited platform triggers a formal notice with three months to comply before recurring penalties begin.

A limited relief mechanism exists: first-time offences within a four-year window may be waived if corrected promptly, and a temporary grace period is under discussion. But the direction of travel is clear, compliance will be enforced, not merely requested.

How to Prepare Your Business

E-reporting readiness is less about one software switch and more about clean, connected data. To stay compliant from day one, businesses should:

Map every transaction type against the e-invoicing and e-reporting scope, so each sale is routed correctly from the outset. Connect beyond billing, ensuring your platform pulls from POS, e-commerce, treasury, and banking sources, not just the ERP invoice module. Confirm your VAT regime and basis (debits vs collection) to fix the right reporting frequency and payment-data obligation. Choose an accredited Plateforme Agréée that handles both e-invoicing and e-reporting in one place. And maintain audit-ready archives in line with France's 10-year retention rule.

Why SMARTeIS Is Built for France

SMARTeIS, developed and maintained by Skill Quotient Technologies, is engineered around France's Y-model from the ground up. It handles both e-invoicing and e-reporting in a single platform, covering B2C, cross-border, and payment-data flows without bolting on separate tools.

Built on the globally trusted Peppol and EN 16931 standards, SMARTeIS generates and validates Factur-X, UBL and CII formats, automates the aggregation and submission of e-reporting datasets to the DGFiP, and adapts automatically as French specifications evolve, at no additional cost. With native connectors for SAP, Oracle, Microsoft Dynamics, Sage and more, your finance teams keep working in familiar systems while SMARTeIS manages validation, transmission, and audit-ready archiving behind the scenes.

Talk to our France e-invoicing expert

Get clarity on e-reporting scope, deadlines, and Y-model integration tailored to your business before the September 2026 deadline.

Frequently Asked Questions

Q1. Is e-reporting the same as e-invoicing in France?

No. E-invoicing applies to domestic B2B transactions exchanged as structured invoices through an approved platform. E-reporting applies to transactions outside that scope, namely B2C sales, cross-border B2B, and certain payment data, where only the data is transmitted to the DGFiP, not a full invoice.

Q2. Do B2C invoices to consumers fall under e-invoicing?

No. Invoices issued to private individuals do not fall within the e-invoicing mandate. However, these B2C transactions are generally subject to e-reporting, which requires transmitting transaction data and, where applicable, payment data, according to your VAT regime and reporting frequency.

Q3. Do foreign companies have to comply with French e-reporting?

Yes. Foreign companies that are VAT-registered in France, even without a permanent establishment, must e-report relevant French-taxable transactions such as cross-border supplies. Under the Loi de Finances 2026, certain deadlines for large and intermediate non-established taxpayers were deferred to September 2027.

Q4. How often must e-reporting data be submitted?

It depends on your VAT regime. Businesses under the standard real regime typically report transaction data every ten days (three times a month) and payment data monthly, while simplified and exemption regimes generally report monthly, each with its own statutory deadline.

Q5. What is the penalty for failing to e-report?

Under the clarified 2026 regime, missing or late e-reporting transmissions carry a fine of €250 per transmission, capped at €15,000 per year, separate from e-invoicing penalties. Using a non-accredited platform can also trigger recurring quarterly penalties after a formal notice period.

Q6. Can one platform handle both e-invoicing and e-reporting?

Yes, and ideally it should. A single accredited Plateforme Agréée such as SMARTeIS manages domestic B2B e-invoicing alongside B2C, cross-border, and payment-data e-reporting, keeping all your French VAT obligations on one compliant, audit-ready system.

Q7. When does the e-reporting obligation start in France?

E-reporting follows the same phased calendar as e-invoicing. It begins on 1 September 2026 for large and mid-sized enterprises, and on 1 September 2027 for small and micro-enterprises. Certain non-established taxpayer obligations were also pushed to September 2027 under the Loi de Finances 2026.

Q8. Which transactions require payment data e-reporting?

Payment data reporting applies only to in-scope transactions where VAT becomes due upon collection of payment, which in practice means mainly services rather than goods. It excludes reverse-charge cases and suppliers who have opted for VAT on debits (TVA sur les débits).

Q9. Is e-reporting transmitted to the DGFiP in real time?

No. Unlike domestic B2B e-invoicing, e-reporting data is not transmitted in real time. It is submitted periodically based on your VAT regime, typically every ten days for the standard real regime or monthly for simplified and exemption regimes, within fixed statutory deadlines.

Q10. What is the difference between a PDP and a Plateforme Agréée (PA)?

They are the same thing. The term PDP (plateforme de dématérialisation partenaire) was officially renamed Plateforme Agréée (PA) under the Loi de Finances 2026. The role is unchanged: a government-accredited platform that validates and transmits your invoices and e-reporting data. Both terms still appear across the market during the transition.