What Is OTA-Compliant E-Invoicing?

Invoices issued, transmitted, and stored in a structured digital format authorized by the Oman Tax Authority under the national program known as Fawtara are referred to as OTA-compliant e-invoicing. The program's primary goal of digitizing and automating invoicing throughout Oman's commercial sector is encapsulated in the word "Fawtara," which is derived from the Arabic meaning invoice.

Sending a PDF by email is not the same as this. A PDF is merely an image of an invoice. A machine-readable document constructed in a predetermined format, usually XML based on the UBL 2.1 standard or PDF/A-3, that systems can automatically evaluate is an OTA-compliant e-invoice. Before it is sent to the buyer, each invoice is validated against tax regulations, has a unique identification and required data fields, and is submitted to the OTA almost instantly.

To put it briefly, an OTA-compliant invoice is designed to be validated, structured, and traceable. Once the rule goes into force, manually typed PDFs or scanned copies are no longer eligible.

How the Fawtara System Works: The Peppol Five-Corner Model

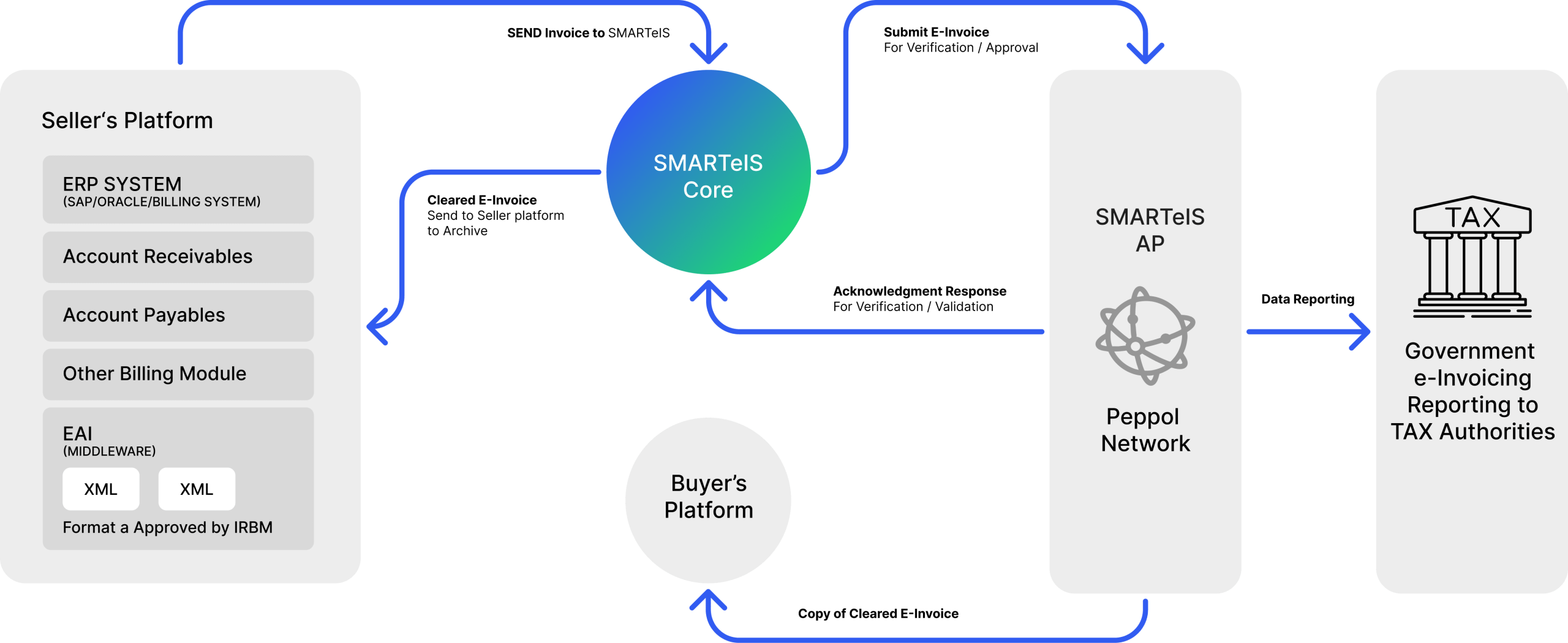

Oman has built Fawtara on the Peppol five-corner model, the same international framework that underpins much of cross-border digital trade. On 7 January 2026, the OTA was officially approved as a Peppol Authority, formally adopting Peppol as the backbone of the system. This makes Oman the third GCC country to mandate e-invoicing, after Saudi Arabia and the UAE.

Here is the practical part that surprises a lot of business owners: under the five-corner model, you cannot connect your ERP directly to the OTA. Direct ERP-to-OTA connectivity is prohibited. Instead, the flow works like this.

Your accounting or ERP system generates a structured invoice. That invoice is sent through an OTA-accredited service provider such as SMARTeIS by Skill Quotient Technologies, known as an Access Point. The OTA validates the invoice in near real time. It is then routed to the buyer's accredited service provider, who delivers it to the buyer. Both parties keep compliant records.

The OTA sits in the network as a fifth corner, retaining full visibility and governance over every invoice exchanged. This gives the tax authority real-time transaction insight while cutting fraud, reconciliation errors, and manual data entry mistakes.

The takeaway: working with an accredited service provider is not optional. It is the only compliant route to exchange invoices under Fawtara.

Who Must Comply, and When

The OTA has confirmed a phased rollout running from 2026 through 2028. Larger taxpayers carry the earliest obligation, and the scope widens over time until it covers essentially every VAT-registered entity. No permanent exemptions have been announced, including for SMEs.

Here is the timeline as it currently stands.

- Pilot phase (February to May 2026): A developer sandbox goes live and the OTA opens applications for Accredited Service Provider certification.

- Phase 1 (August 2026): Mandatory compliance begins for roughly 100 of the largest taxpayers already notified by the OTA. These businesses must issue and receive e-invoices through Fawtara. B2G transactions for selected large taxpayers also begin in this window.

- Phase 2 (early 2027): The mandate extends to the remaining large VAT-registered taxpayers based on revenue thresholds set by the OTA.

- Phase 3 (mid to late 2027): All remaining VAT-registered businesses, including small and medium enterprises, must comply.

- Phase 4 (2028): Government-related transactions come fully into scope, completing the nationwide framework.

A word of caution on dates. The 2027 milestones should be treated as indicative rather than final, since several technical and scheduling details remain subject to OTA confirmation. The direction of travel, however, is settled. If you are VAT-registered in Oman, your turn is coming. The only variable is exactly when.

What a Compliant E-Invoice Must Contain

The OTA's data dictionary defines the anatomy of a compliant invoice in detail, including which fields are mandatory and which are conditional. Standard e-invoices require a substantial set of mandatory fields, with additional conditional fields layered on top, covering multiple document types and transaction types across B2B, B2C, and B2G, for both rated and exempt supplies.

At a minimum, a compliant invoice must include the seller and buyer details, both parties' VAT identification numbers (VATINs), line items, the VAT rate and amount, timestamps, and a unique identifier (UUID). Goods typically require HS codes. Invoices must be issued in the approved structured formats, validated against the OTA's rules before submission, and they cannot simply be cancelled. Corrections are handled through credit notes instead.

One important nuance from the most recent specifications: features such as QR codes, digital signatures, and invoice hashing that appeared in earlier draft documentation were removed from the mandatory field set in the April 2026 PINT-OM specification. This is a good illustration of why you should track the OTA's technical releases closely rather than relying on older guides, since the requirements are still being refined.

You must also retain e-invoices in digital form for 10 years from the end of the relevant year, with integrity checks in place, and ensure your archiving respects Oman's data residency rules.

Why Every Oman Business Must Care

It is tempting for a smaller business to assume this is a problem for large enterprises in 2026 and to revisit it later. That is a costly assumption. Here is why this matters for you now, regardless of size.

- The penalties are real and codified

Non-compliance is not a minor administrative issue. It carries financial, legal, and operational consequences under Royal Decree No. 121/2020, the Oman VAT Law, and its Executive Regulations. Under Article 100 of the VAT Law, deliberately failing to issue a tax invoice when required can result in a fine ranging from OMR 1,000 to OMR 10,000, imprisonment of two months to one year, or both. Critically, this is not limited to issuing no invoice at all. It also covers issuing an invoice in a non-approved format, such as paper or PDF, after the mandate takes effect, or omitting mandatory fields.

- The quieter costs hurt more

Beyond fines, input tax credits may be denied if supporting invoices were not OTA-validated, which directly affects your cash flow. Repeat compliance issues can raise your audit risk profile and invite deeper investigation. These consequences rarely make headlines, but they often damage a business more than the fines themselves.

- Compliance is now a board-level concern

Under Oman's VAT framework, responsibility extends to leadership. Executives cannot fully delegate accountability to the IT team or an external vendor. Repeated failures to issue compliant invoices can be read as weak internal controls rather than isolated mistakes. Compliance, or imtithal, has moved from the accounts department to the boardroom.

- Most failures are avoidable

The reassuring part is that the majority of penalties stem not from misconduct but from avoidable gaps: continuing to issue paper or PDF invoices after the mandate is active, running outdated billing software that cannot produce structured XML or JSON, working with non-accredited service providers, or missing mandatory fields like UUIDs. Every one of these is preventable with the right preparation.

How to Prepare for OTA-Compliant E-Invoicing

You do not need to solve everything at once, but you do need to start. Here is a practical sequence.

- Assess your ERP and billing software: Confirm whether your current system can generate and export structured invoices in XML (UBL 2.1) or PDF/A-3, and whether it can connect to external APIs. If it cannot, you need an upgrade or middleware.

- Clean up your master data: Validation will reject invoices with incomplete or inaccurate data. Make sure buyer and seller legal IDs, VAT treatment, and product HS codes are accurate so mandatory fields populate correctly.

- Choose an accredited service provider: Since direct OTA connection is not permitted, select an ASP that supports the Peppol five-corner model and the PINT-OM specification. ASP accreditation began in May 2026, so this is an active decision, not a future one.

- Use the sandbox and pilot windows: Once test environments are available, validate your message schemas, field population, and high-volume throughput before your phase goes live. Catching errors in testing is far cheaper than rejected invoices in production.

- Set up compliant archiving: Put 10-year digital retention in place with integrity controls and ensure your storage meets Omani data residency requirements.

- Monitor OTA announcements: The specifications are still being finalized in places. Track official releases so you are working from current requirements, not last year's draft.

Final Word

In Oman, OTA-compliant e-invoicing is no longer an option. It is an ongoing regulatory change with a clear penalty system and a predetermined course. The rule first applied to large taxpayers in August 2026, but by 2028, it will apply to almost all VAT-registered businesses.

Errors in compliance can have serious consequences, such as rejected invoices, refused tax credits, fines, and even jail time. The majority of the expense of doing it correctly comes from preparation: the appropriate software, precise data, an approved service provider, and a routine of monitoring OTA updates. The deadline will be viewed as a formality by companies that start early. Those who wait will be rushing. The time has already begun to run.

Avoid making your compliance deadline an emergency. Discover Oman e-invoicing with us to prepare your business for OTAs and begin the journey toward seamless, penalty-free compliance.

Frequently Asked Questions

1. What is the best e-invoicing software in Oman for Fawtara compliance?

The best e-invoicing software in Oman is one that's built specifically around the OTA's five-corner Peppol model rather than retrofitted from a generic invoicing tool. Look for a Fawtara compliant software that offers native PINT-OM alignment, real-time ERP integration, and pre-validation before submission, since this is what separates a genuinely OTA compliant e-invoicing platform from one that simply claims compliance.

2. How is Peppol e-invoicing Oman different from regular invoicing software?

A Peppol e-invoicing Oman solution doesn't just generate digital invoices - it routes them through the Peppol network's standardized exchange architecture, with the Oman Tax Authority sitting as the fifth corner for real-time validation. Regular invoicing software that simply emails a PDF or exports a spreadsheet doesn't meet this structural requirement, regardless of how polished the output looks.

3. Is there a leading e-invoicing solution in Oman built for SMEs specifically?

Yes. While much of the early conversation centers on large taxpayers, e-invoicing software for SMEs Oman businesses need should offer simpler onboarding, lower upfront integration cost, and scalable pricing, since SMEs face the same OTA compliant e-invoicing requirements under Phase 3 without the in-house IT teams larger enterprises have.

4. What makes a provider a "pre-approved" e-invoicing service provider in Oman?

A pre-approved e-invoicing service provider Oman recognizes has already passed the OTA's accreditation testbed, met the reduced paid-up capital threshold, and demonstrated it can operate within the Peppol five-corner model as an Access Point. Working with a pre-approved provider, rather than one still mid-accreditation, removes a layer of timeline risk for your own go-live date.

5. Can I find an e-invoicing system in Oman that also works across other GCC countries?

Several Fawtara-ready platforms are built as multi-jurisdictional e-invoicing solutions, supporting Oman alongside Saudi Arabia's ZATCA and similar Peppol-based frameworks elsewhere in the GCC. This matters most for businesses with cross-border operations who don't want a separate e-invoice system in Oman from the one used in their other markets.

6. What's the difference between an e-invoicing solution and just an "e-invoice generator"?

A true e-invoicing solution for Oman covers the full lifecycle: invoice generation in XML/UBL 2.1, ASP routing, OTA validation, buyer delivery, acknowledgment tracking, and 10-year compliant archiving. A basic e-invoice generator may only produce the structured file but leave the transmission, validation, and storage obligations entirely up to you.

7. How do I evaluate the top e-invoicing software in Oman before choosing one?

Compare providers on PINT-OM and Peppol PINT alignment, native ERP integration (SAP, Oracle, Microsoft Dynamics, or your accounting platform), accreditation status with the OTA, archival capability for the mandated retention period, and proven track record with the Oman Tax Authority e-invoicing rollout, rather than choosing on price or marketing claims alone.

8. Does the OTA maintain an official list of approved e-invoicing providers?

The Oman Tax Authority publishes accreditation status through its tax portal as part of the Fawtara e-invoicing rollout, and businesses should verify a provider's current accreditation directly rather than relying solely on the provider's own claims, since accreditation has been an active, evolving process since May 2026.

9. What should I look for in an e-invoicing system for Oman if I'm a first-time adopter?

First-time adopters under the Oman e-invoicing mandate should prioritize ease of ERP connection, a vendor who handles ongoing PINT-OM specification updates on your behalf, transparent onboarding support, and a sandbox/testing environment, since the technical specifications are still being refined and you don't want to manage that complexity internally.

10. Is switching e-invoicing software providers difficult once I've integrated one?

It depends on how the original integration was built. A provider using standardized API connections and clean data mapping makes switching easier; one using deeply custom, non-standard integrations can make migration costly. This is worth confirming upfront with any e-invoicing solution in Oman you're evaluating, before committing to a long-term contract.